Are You Paying Too Much for Convenience? A Look Inside Zepto, Blinkit, and Instamart

It was 10:30 PM, and the house was finally quiet. The kind of silence parents wait for all day had just settled in when the fridge opened, and there it was, the problem. No milk for the morning.

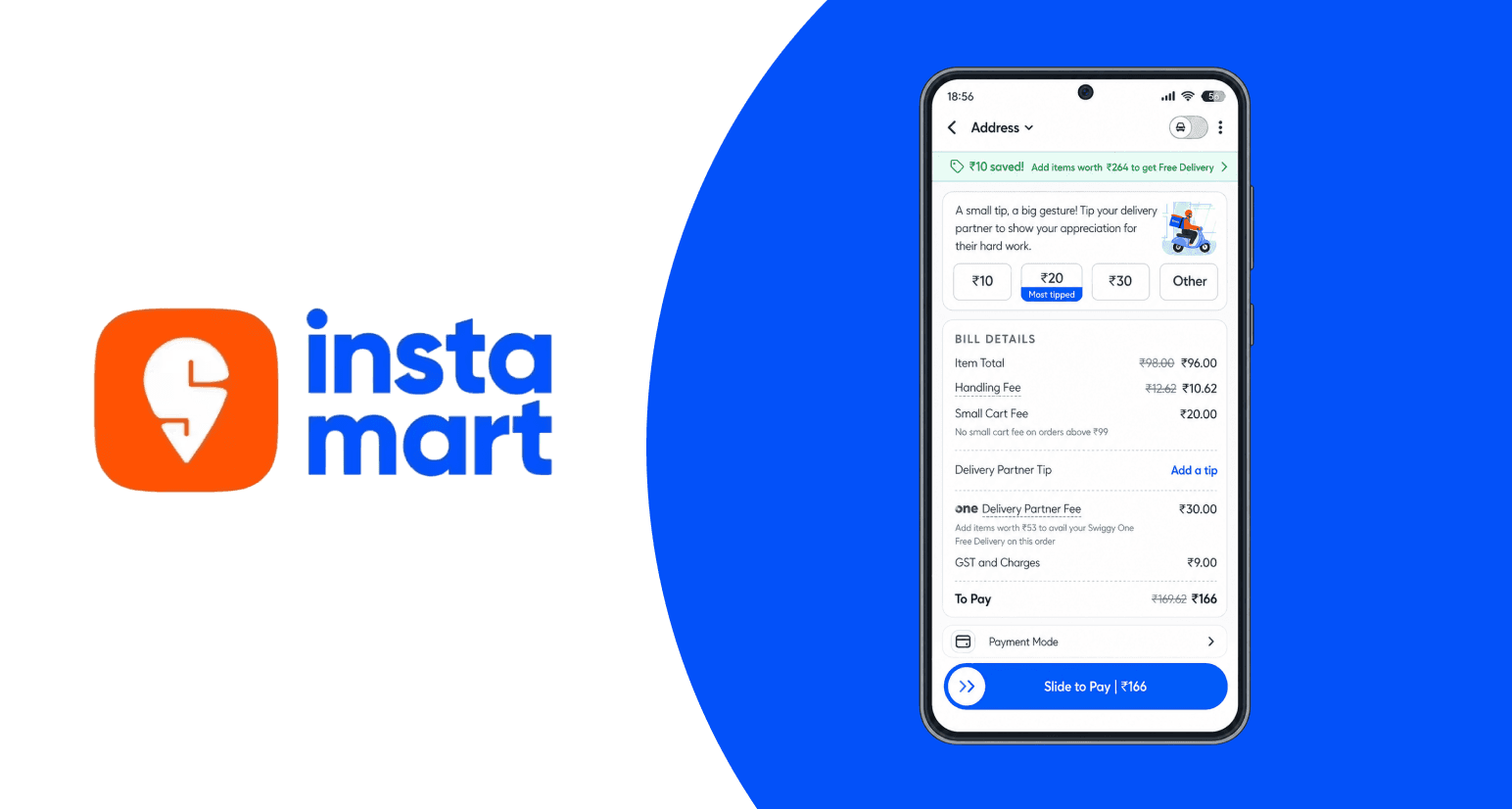

A quick tap on the phone and within seconds, milk was added to the cart. Then came a packet of chips and a cold drink for their child. The total bill showed ₹166, and he tapped “Pay Now” without a second thought. It felt too small to question, too convenient to resist, and too quick to even notice what had just happened. By 10:40 PM, the doorbell rang, and the delivery arrived in just 10 minutes.

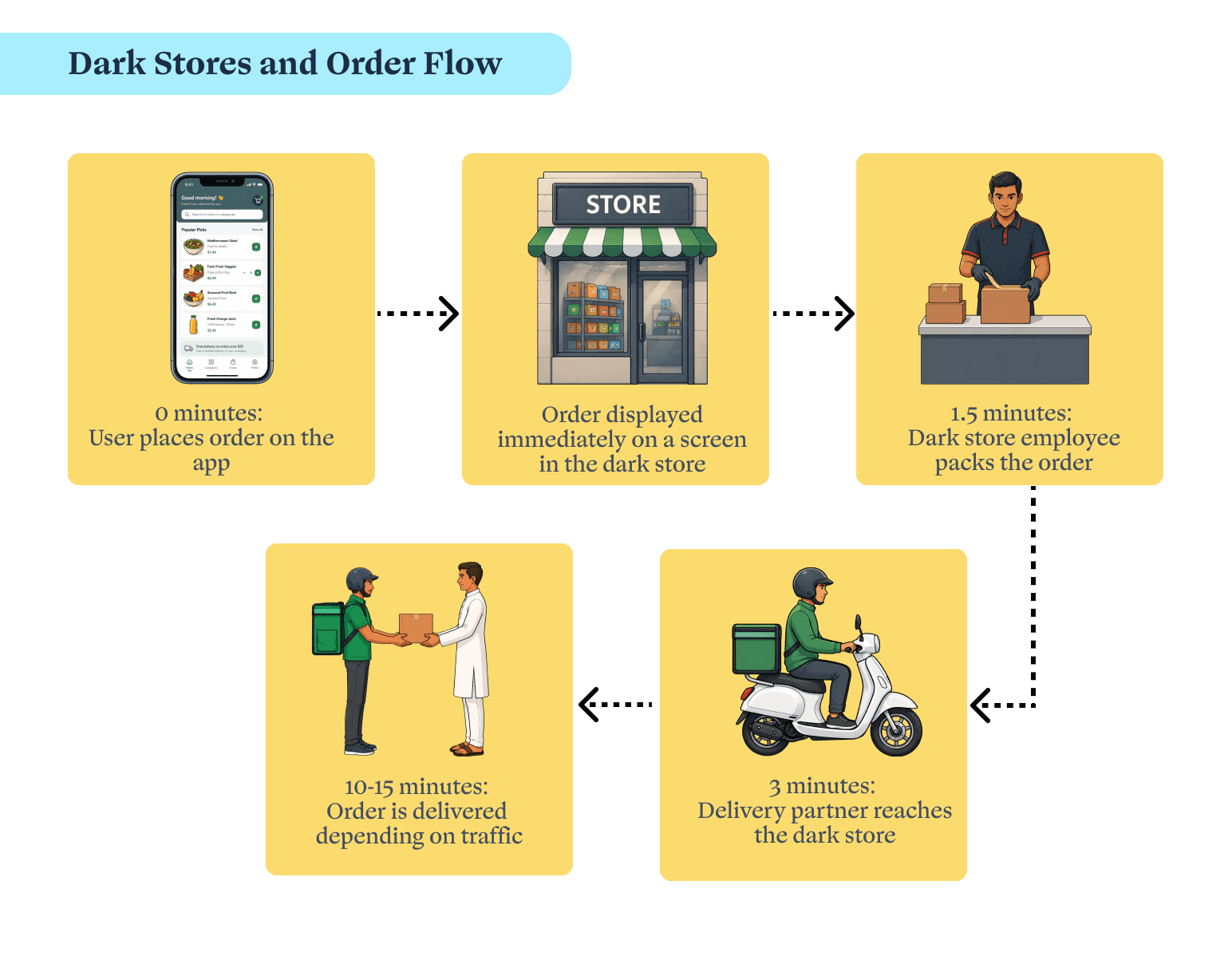

Behind that ten-minute delivery was an entire system working silently in the background. These apps do not rely on traditional retail stores. They operate through what are called dark stores, small warehouses located within neighbourhoods, stocked with high-demand products and optimised only for speed, not for walk-in customers.

This system is what makes it possible to deliver thousands of items in minutes, but it also comes with its own cost structure. Inventory holding, last-mile logistics, and hyperlocal operations all add layers of expense that are eventually built into the price you see on your screen.

Now what if that ₹166 was not really ₹166, and what if this exact moment is happening in millions of households across India every single day? Because behind that one harmless order lies a silent financial pattern that most families have not yet recognised.

The Rise of Convenience, and Its Quiet Cost

A few years ago, ordering groceries online was occasional. In 2026, it has become routine.

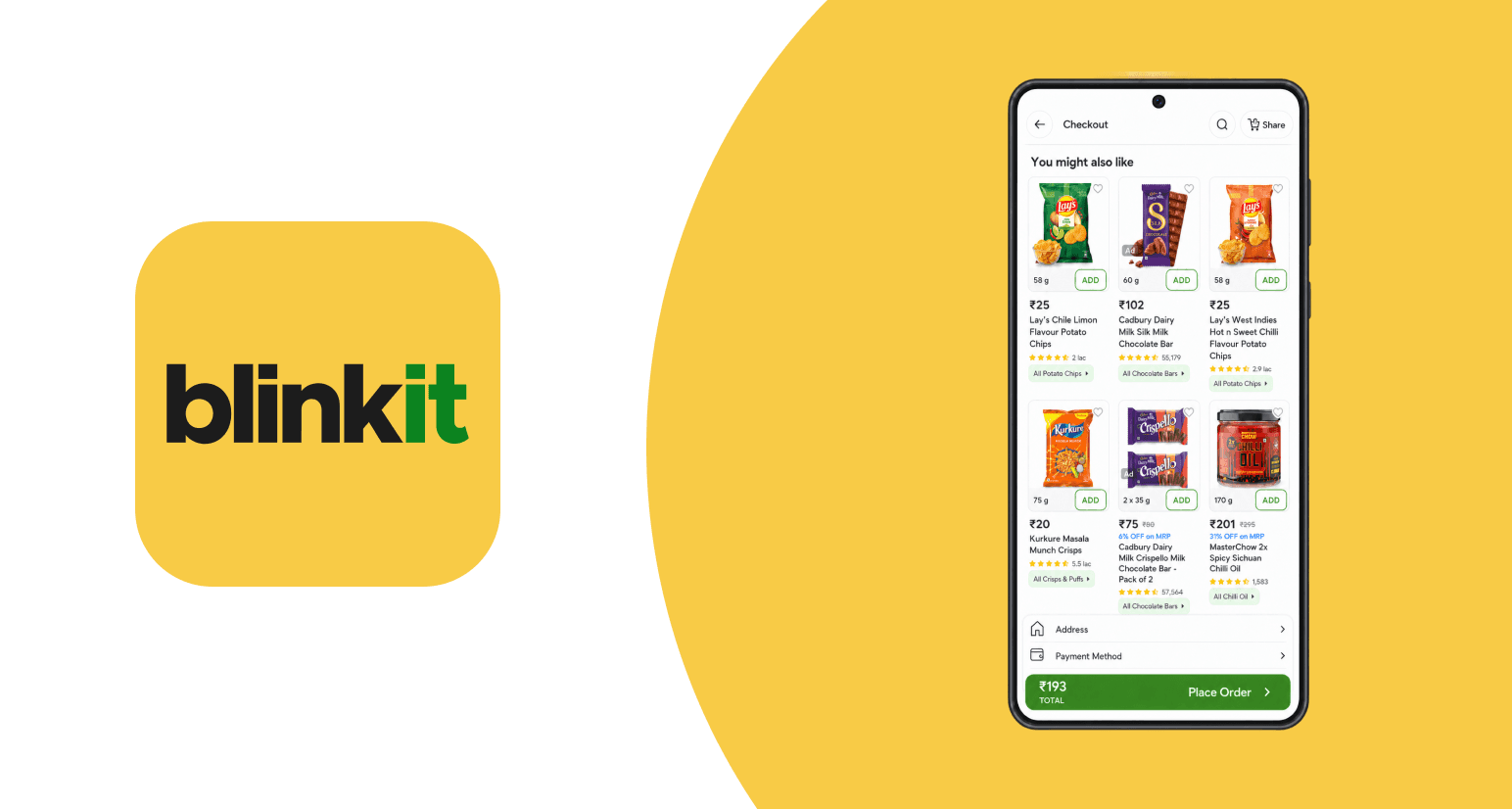

Apps like Zepto, Blinkit, and Instamart have evolved far beyond groceries. You can now order over 30,000 products, from daily milk to electronics, all delivered within minutes. It feels like progress, like efficiency, like modern living at its best.

But convenience is never free, and the idea of convenience tax on households is becoming increasingly relevant. Every order comes with layers of hidden costs. Delivery fees, handling charges, surge pricing, and slightly inflated product prices quietly build into the final bill.

Individually, these charges feel insignificant, but together they create something much larger. And that is where the real story begins.

What Is the 15% Lifestyle Tax?

Let us simplify this with numbers that everyone understands.

If a household spends ₹20,000 per month on quick commerce apps, which is not uncommon in urban India today, and if we assume an average 15% markup across fees and inflated prices, that is ₹3,000 quietly slipping away every month.

That is ₹36,000 a year. That is not just spending. That is a leak. This is what experts are now referring to as the problem of quick commerce hidden costs, where the illusion of affordability hides the reality of cumulative loss.

And once you see this number, it becomes impossible to ignore what it could have become instead.

Impulse Inflation As The Invisible Enemy

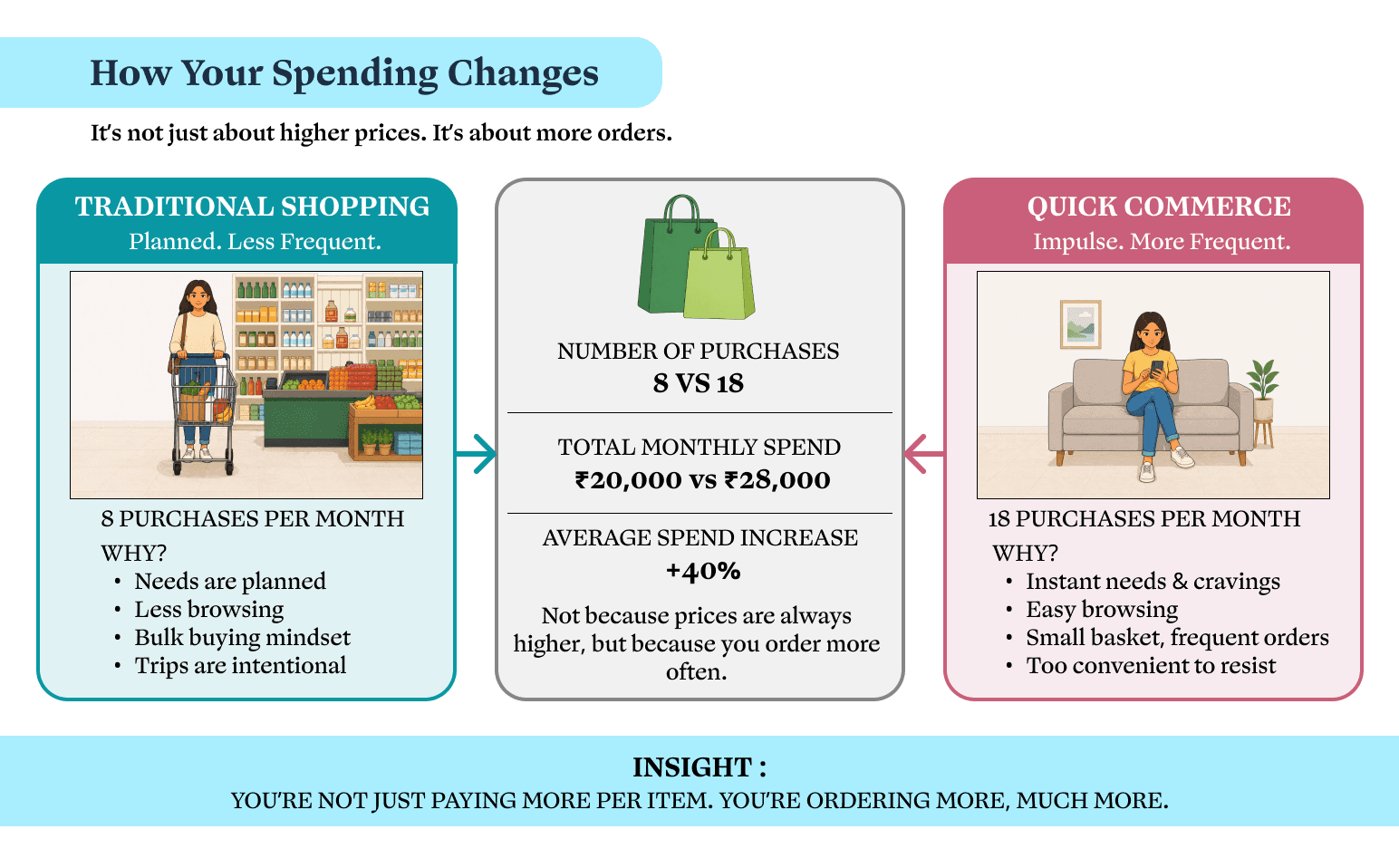

There is another layer to this story, something even more subtle. Quick commerce does not just make things expensive. It makes you buy more.

The moment delivery time drops to 10 minutes, the decision-making process disappears. You are no longer planning purchases. You are reacting to cravings, moods, and small inconveniences.

The real shift is not just in pricing, it is in behaviour. You may open an app to buy essentials, but you leave with extras. This is not accidental. Features like “people also bought,” “complete your basket,” and “free delivery above ₹199” are designed to influence decisions.

This leads to what economists are calling impulse spending habits, where frequency of purchase increases, even if individual order sizes remain small.

You are not just paying more per order. You are ordering more often. And this is where the cost doubles quietly.

Why Your Brain Loves It, and Your Wallet Does Not

The human brain is wired to prefer instant gratification. When you can solve a problem in ten minutes, your brain rewards you with a small dose of satisfaction. This is why quick delivery spending impact is not just financial, but psychological.

You start associating comfort with ordering. You begin to outsource small efforts. And slowly, convenience becomes a habit, not a choice. But habits compound. And when spending habits compound, they do not stay small for long.

The Math Most Families Are Missing

Let us go back to that ₹3,000 per month. If instead of spending that amount on convenience premiums, a person invested it in a mutual fund SIP with a modest return of 10% annually, here is what happens:

₹3,000 per month becomes approximately ₹6.8 lakh in 10 years. ₹3,000 per month becomes over ₹23 lakh in 20 years. This is the real cost of the phenomenon of household spending leaks in India.

You are not just losing ₹3,000. You are losing what that ₹3,000 could have become. And that is where this story shifts from spending to opportunity loss.

The Hidden Layers Inside Every Order

Let us break down a typical quick commerce bill:

Product MRP inflated by 5 to 10%

Delivery fee: ₹15 to ₹40

Handling charge: ₹5 to ₹20

Surge pricing during peak hours

Combined, this leads to the reality of q-commerce price markup in India, where the actual cost of goods is significantly higher than traditional retail or even standard e-commerce.

But because these costs are fragmented, the consumer rarely notices the full impact. And what we do not notice, we rarely question!

Why This Feels Harmless but Isn’t

Most families do not track small expenses. A ₹30 delivery fee does not trigger concern. A ₹10 markup does not feel worth thinking about.

But repeated over dozens of transactions, these small numbers form a pattern. This is the essence of online grocery premium charges in India, where micro-costs accumulate into macro-impact.

And once this becomes a habit, it becomes part of your monthly lifestyle.

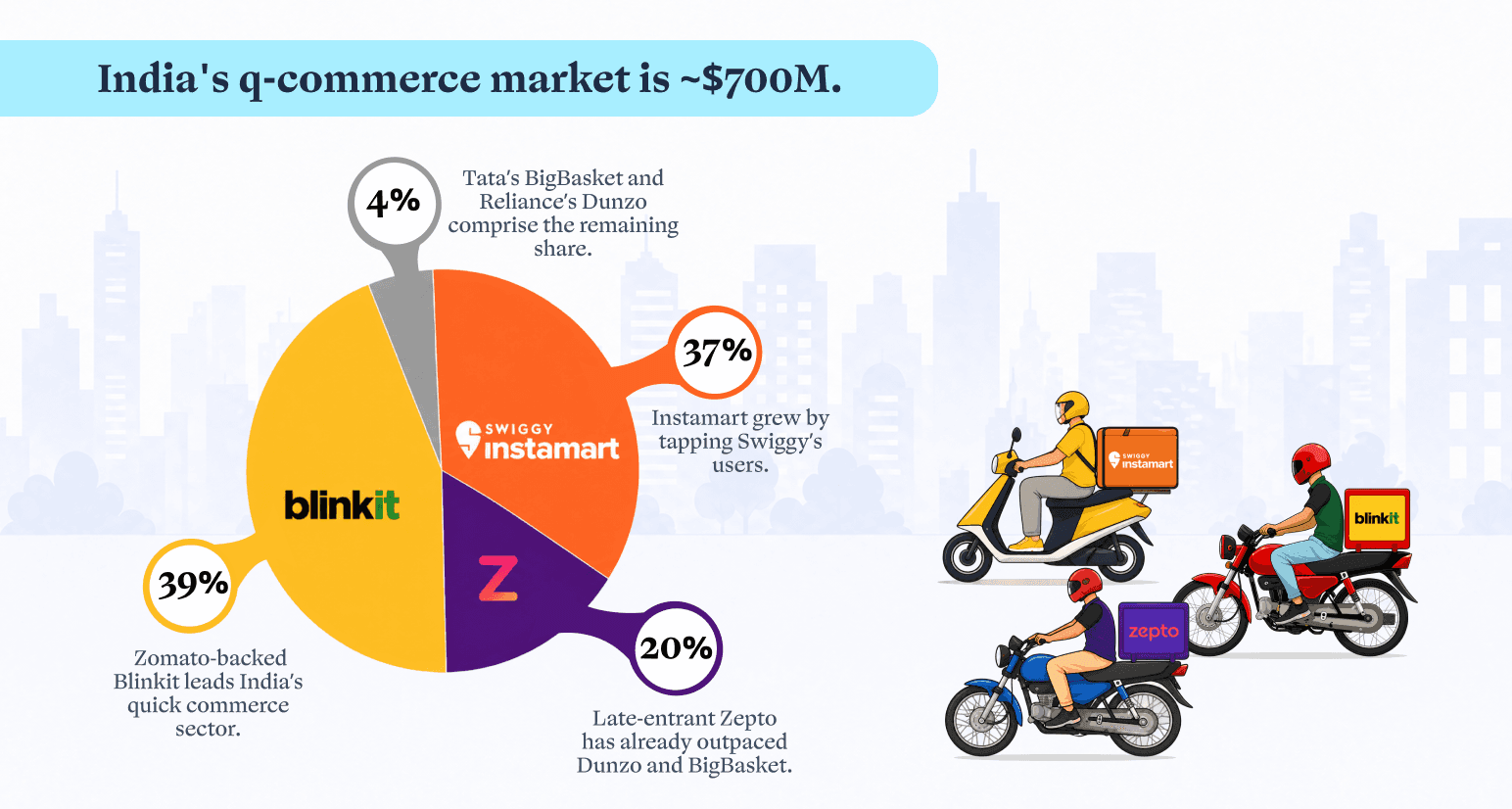

The Bigger Economic Picture

India’s quick commerce market is projected to cross $5 billion by 2026, growing at over 25% annually. This growth is powered not just by demand, but by behavioural shifts. Consumers are trading time for money more frequently than ever before.

This aligns with the broader 10 minute delivery economics in India, where companies optimise for speed, and consumers unknowingly pay the premium for it.

But the question is not whether the system works. The question is whether it works for your family.

The Family Budget Impact No One Talks About

For a middle-income household, ₹3,000 a month is not insignificant. It could cover:

A child’s extracurricular classes

Health insurance premium top-up

SIP contribution for education

But when this amount is absorbed into daily convenience, it disappears without accountability. This is the true cost of the convenience tax on households.

And once you recognise this, the next question becomes unavoidable.

Should You Stop Using These Apps?

Not at all. Quick commerce is not the enemy. Unconscious usage is. The goal is not to eliminate convenience, but to control it.

Here are simple strategies:

Set a monthly budget cap for quick commerce

Use it for emergencies, not routine purchases

Compare prices before ordering

Track your monthly spend consciously

Because awareness is the first step toward control. And control is what converts spending into strategy.

The Final Thought That Changes Everything

The next time you place a quick order, pause for five seconds. Not to cancel it, but to understand it. Ask yourself: is this convenience worth the long-term cost?

Because the most dangerous expenses are not the big ones. They are the small ones you never question. And that is where the real financial story begins.

Pockvue Solutions Private Limited

#1, CRE Spacez, 2nd Floor, 14th Main Road,

Sector 5, HSR Layout, Bengaluru - 560102