A family vacation usually begins with a spreadsheet.

Flights for four people. Hotel rooms. Airport cabs. Meals. Foreign currency. A few emergency purchases that nobody planned for. By the time the trip ends, the real cost often feels much larger than the number parents had in mind when they first searched for tickets.

Now imagine a different version of the same trip.

The money is still spent. The flights are still booked. The hotel is still paid for. But instead of that spend disappearing after the payment, it quietly creates a second layer of value. A pool of points. A possible flight redemption. A hotel partner transfer. Lounge access. An airport ride that does not need another cab booking. That is the idea behind the 28% cashback equivalent conversation around the HSBC TravelOne Credit Card.

The important word is “equivalent”. This is not ₹28,000 being credited into your bank account for every ₹1 lakh you spend. It is not normal cashback. It is a travel-value strategy where the final benefit depends on how the cardholder earns, transfers, and redeems.

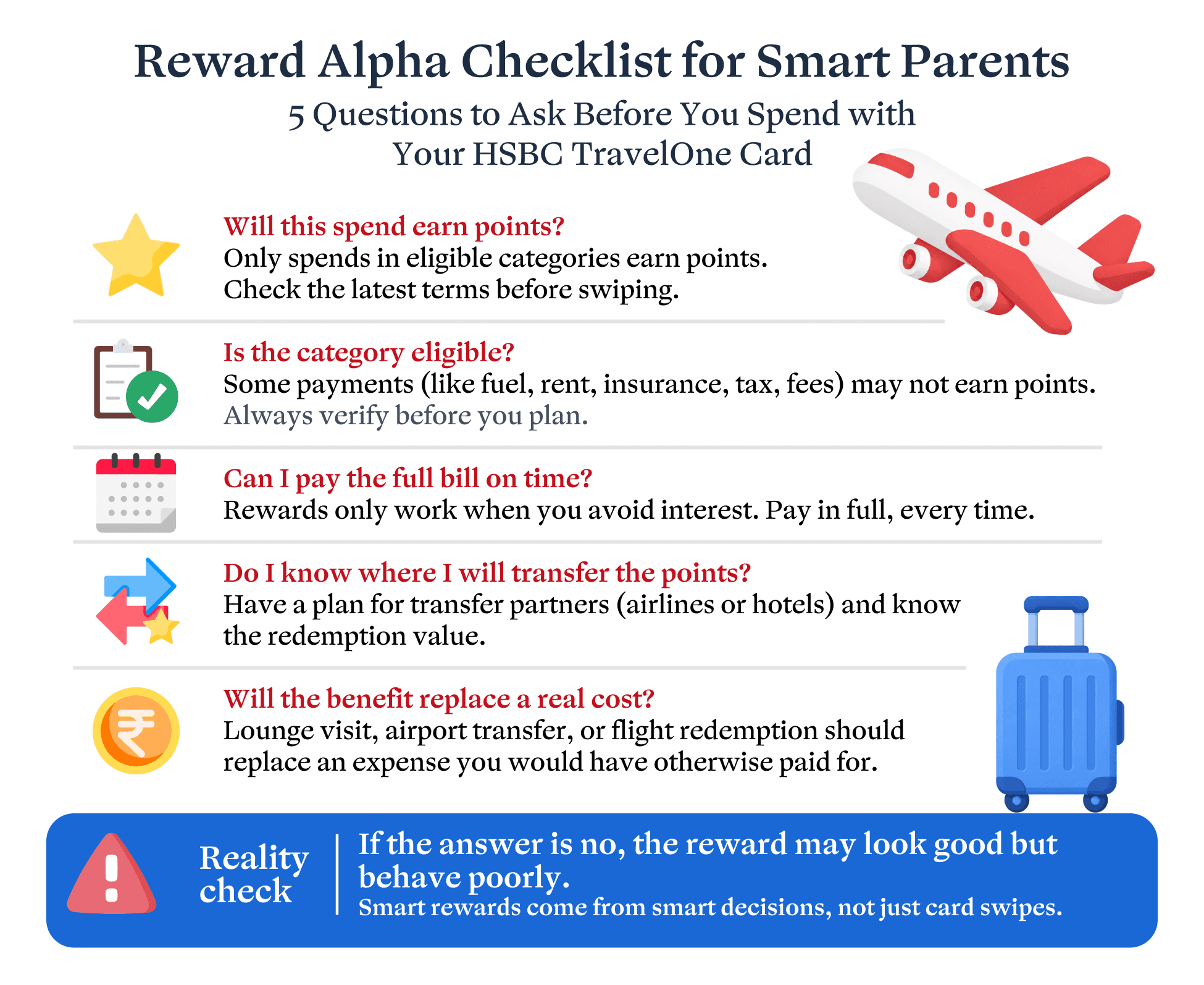

HSBC’s TravelOne rewards page says the card earns 4 reward points per ₹100 on flights, travel aggregators, and foreign currency spends, 2 reward points per ₹100 on other eligible spends, 10,000 bonus reward points on annual spends above ₹12 lakh, and instant 1:1 conversion of reward points to air miles through the HSBC India app.

That is the base of the “28%” story. But the real story begins when a family stops thinking like a cashback user and starts thinking like a travel planner.

The cashback habit most families never question

Cashback is easy to love because it is simple.

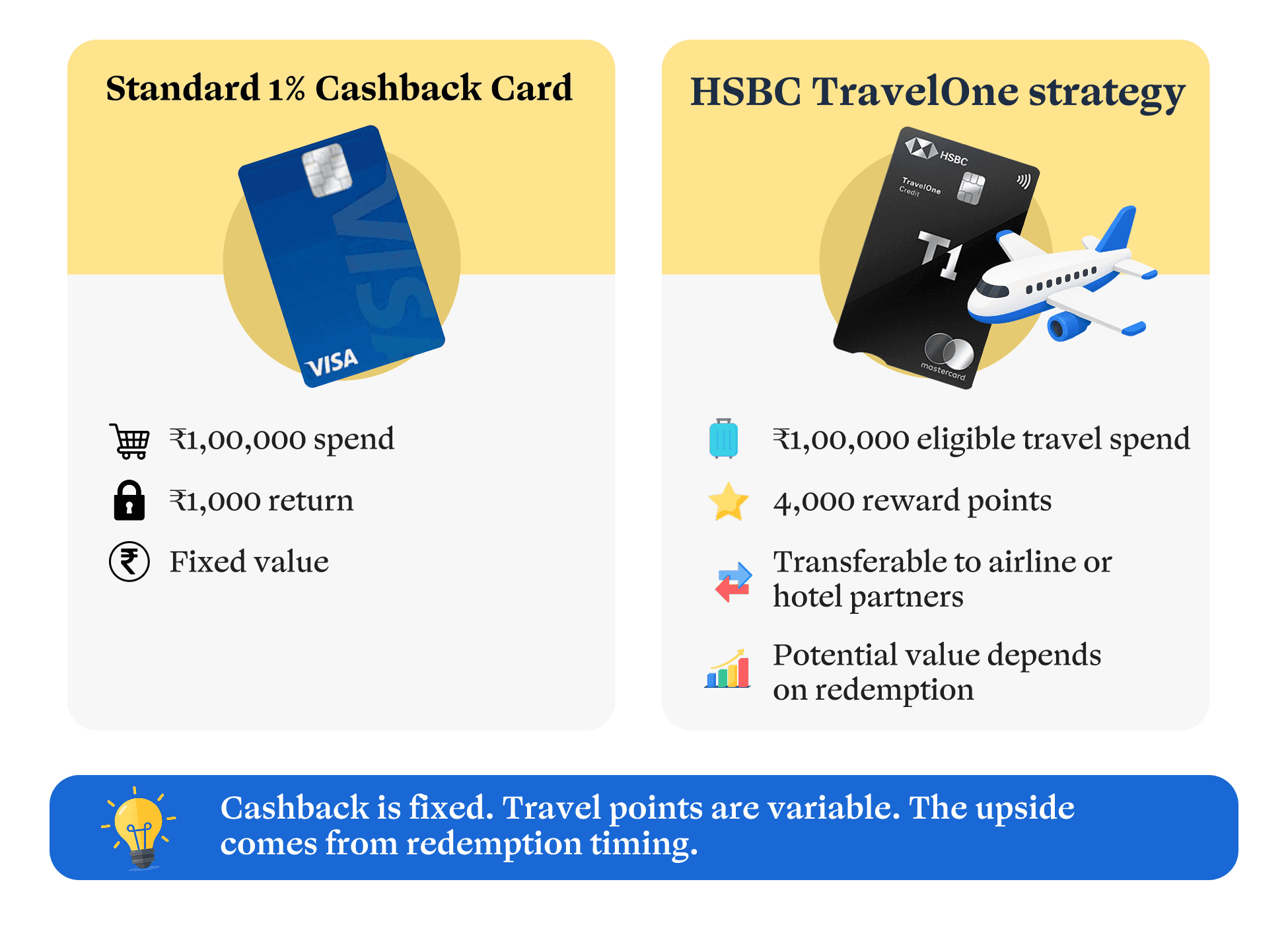

A standard 1% cashback card gives ₹1,000 on ₹1 lakh spend. There is no strategy, no loyalty programme, and no need to compare airline partners. The return is small, but it is visible.

Travel rewards are different.

They look weaker at first because they appear as points. Points do not feel as satisfying as money. They sit inside an app, waiting to be moved somewhere useful.

That is exactly why many people underestimate them.

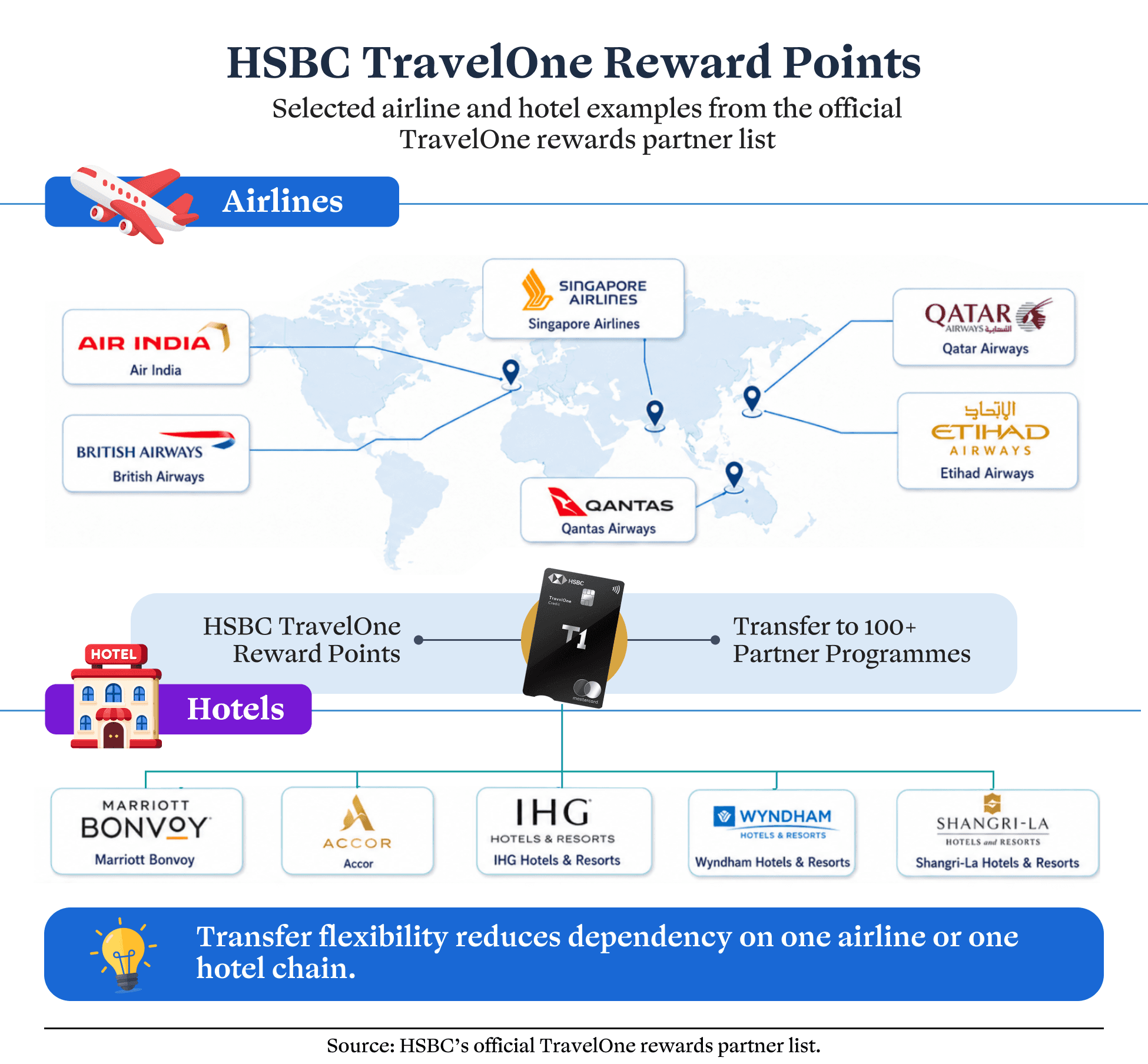

A reward point is not valuable because it exists. It becomes valuable when it is transferred to the right partner and redeemed at the right moment. HSBC lists airline partners such as Air India Maharaja Club, Singapore Airlines KrisFlyer, British Airways Executive Club, Etihad Guest, Qatar Airways Privilege Club, Japan Airlines Mileage Bank, Qantas Frequent Flyer, and others, with many programmes available at a 1 reward point to 1 mile conversion.

That air mile transfer ratio is the hidden engine of the card. It lets a family convert card spending into travel currency. Once that happens, the value is no longer limited to a fixed 1% cashback number.

The ₹1 lakh example

Let us say a parent spends ₹1,00,000 on eligible travel bookings. With a regular 1% cashback card, the return is ₹1,000. With the HSBC TravelOne earning structure, that same travel spend creates 4,000 reward points.

If those 4,000 points are used casually, the value may be average. But if they are transferred to a flight or hotel partner where cash prices are high, the outcome can become far more interesting.

For example, school holidays often push up airfare and hotel rates. A route that feels affordable in February can become expensive in May. A hotel that looks reasonable on a weekday can become costly during a long weekend. In those moments, a well-timed points redemption can offset a cost that would otherwise be paid in cash.

This is where the “28%” figure enters the picture. It’s not saying every ₹1 lakh spend automatically becomes ₹28,000 in cash. It is saying that in a high-value travel scenario, the combined worth of points, milestone rewards, lounge access, airport transfers, and other usable perks may create a perceived return that reaches that level.

So the smart question is not, “How much cashback did I get?” The better question is, “How much future travel did this spend help create?”

The annual spend strategy

The card becomes more powerful when the family looks beyond one transaction.

Suppose a household plans its annual travel and lifestyle spends carefully. Flights, hotels, foreign currency expenses, and eligible purchases are directed through the card without increasing the family’s actual consumption.

At ₹12 lakh annual spend, the milestone benefit becomes relevant. HSBC states that cardholders earn 10,000 bonus reward points after spending more than ₹12,00,000 in a year. If a large part of that annual spend falls into accelerated travel categories, the family has a stronger points base. The milestone bonus then works like an extra push at the top of the ladder.

This is the difference between spending randomly and spending with a rewards map. Random spending creates scattered benefits. Planned spending creates a travel fund. That is the heart of optimizing credit card points. The goal is not to spend more money. The goal is to make planned expenses more productive.

How the 28% value stack is built

The TravelOne math works in layers.

The first layer is accelerated earning on eligible travel and foreign currency spends.

The second layer is the ability to move points to airline and hotel partners. HSBC lists hotel options including Accor Live Limitless, IHG One Rewards, Marriott Bonvoy, Shangri-La Circle, and Wyndham Rewards, with some available at a 1 reward point to 1 loyalty point ratio.

The third layer is the annual milestone bonus.

The fourth layer is travel comfort. HSBC’s product page lists 6 local and 4 international airport lounge visits every year for the TravelOne card.

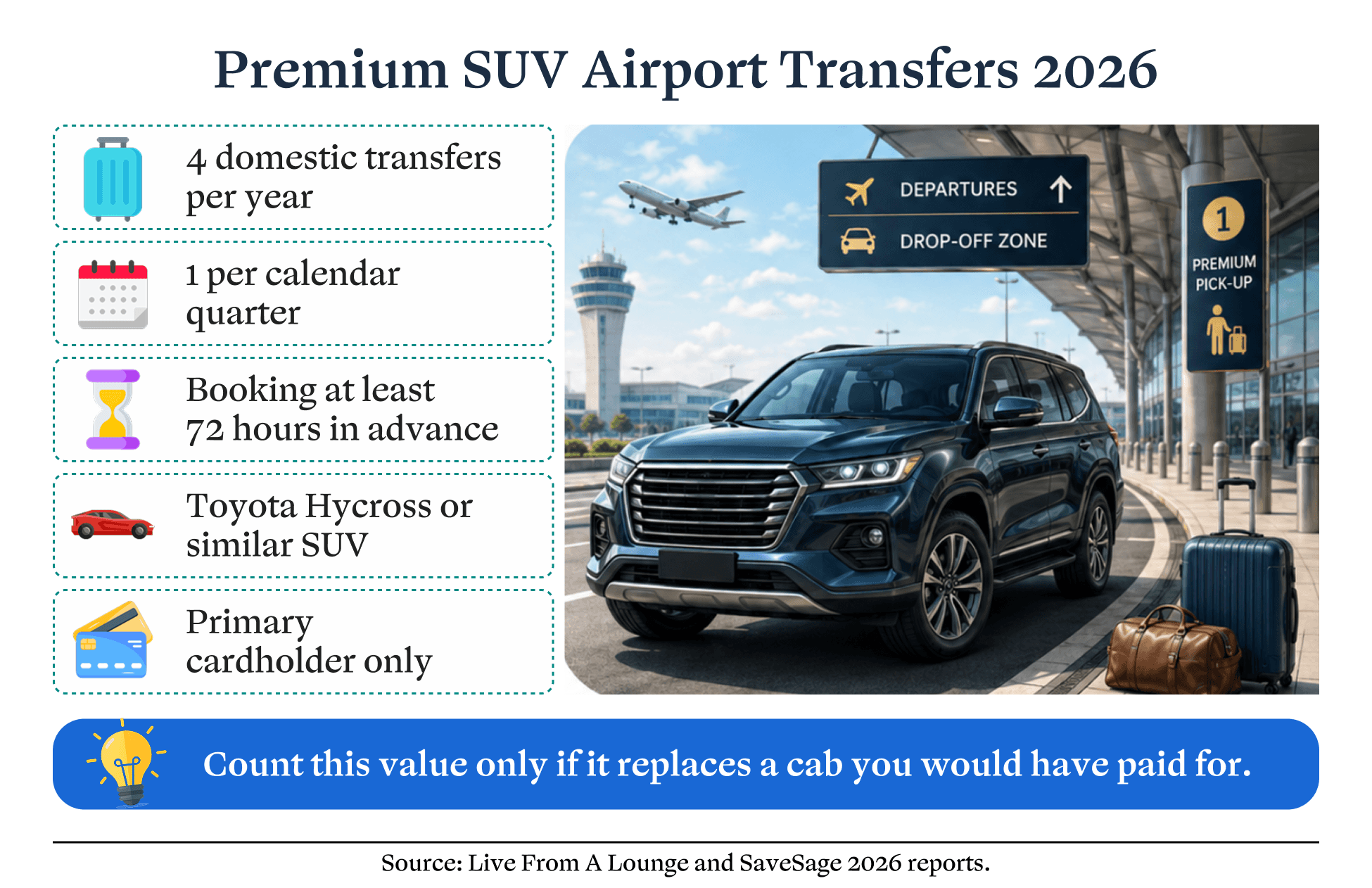

The fifth layer is convenience value. For 2026, Live From A Lounge reported that primary TravelOne cardholders get 4 complimentary domestic airport transfers, one per quarter, with booking required at least 72 hours in advance. The same report notes that the cars are Toyota Hycross or similar premium SUVs, subject to passenger and baggage limits.

This is why the final number must be understood as a value stack. A family does not get 28% from one feature. The figure becomes possible only when several benefits are actually used and replace expenses the family would otherwise have paid for.

If a lounge visit saves a paid meal at the airport, it has value. If a complimentary SUV transfer replaces an airport cab, it has value. If transferred points reduce the cash cost of a flight or hotel, they have value. If a benefit would never have been used, it should not be counted. That is the honest version of the rewards math.

The Time Value of Loyalty Points

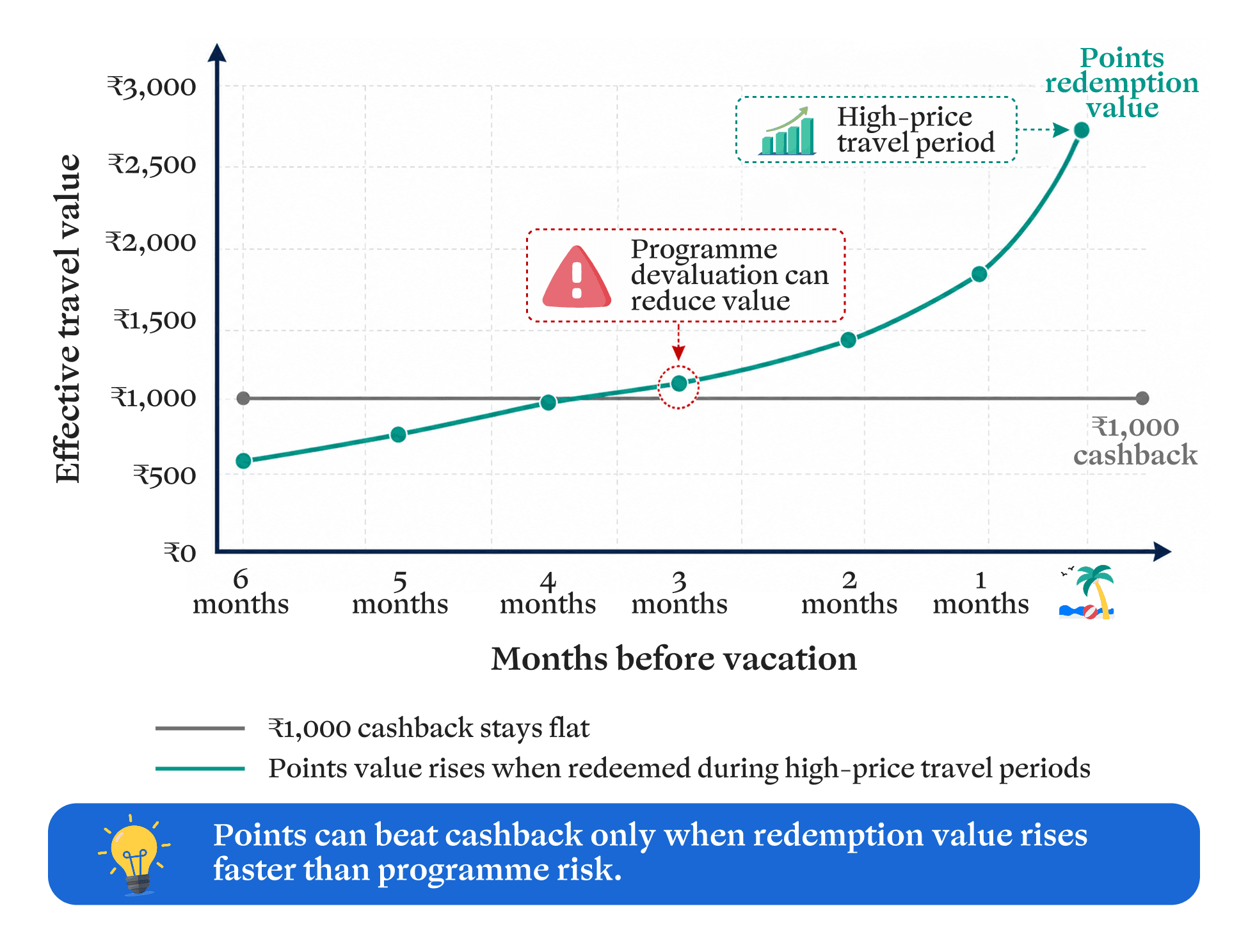

Money loses purchasing power when prices rise. Travel costs can behave the same way, often more sharply.

Flights during school vacations. Hotels during festive weekends. International trips planned around summer holidays. These are moments when demand can make travel expensive very quickly.

Loyalty points can work like a partial inflation hedge when they are earned before the trip and redeemed when cash prices are high. A family that has already built a points balance may not feel the full pressure of peak-season pricing.

But there is a second side to this idea. Points are not bank deposits. Airlines and hotels can change programme rules, redemption rates, availability, and partner terms. That means points should not be hoarded without a plan.

The smart approach is to earn with purpose and redeem with timing.

Why the airport transfer benefit matters

Some card benefits are invisible. A points transfer happens inside an app. A redemption chart is read on a screen. A hotel loyalty balance looks like a number.

An airport transfer is different. It is physical. The car arrives. The luggage fits. The family leaves for the airport without waiting for a cab or worrying about surge pricing.

That is why the reported 2026 premium SUV transfer benefit adds emotional weight to the TravelOne story. SaveSage also reported that the 2026 service includes 4 complimentary domestic airport transfers for primary cardholders, valid from 1 January to 31 December 2026, with vehicles such as Toyota Hycross or similar premium SUVs.

This benefit does not change the points equation by itself. It changes the experience around the equation. For a family with children, elderly parents, or multiple bags, a reliable airport transfer can feel more valuable than a discount buried inside a statement. That is where premium cards build loyalty. They do not just reduce cost. They reduce friction.

The Reward Alpha mindset

In investing, alpha means the extra return generated through better decisions. In credit card strategy, Reward Alpha means the extra travel value created by choosing the right card for the right spend. A cashback card gives certainty. A travel-rewards card gives optionality.

Certainty is useful when the user wants a guaranteed rupee return. Optionality is useful when the user understands partners, travel timing, and redemption value. The HSBC TravelOne card belongs to the second category.

Its upside depends on behaviour. A disciplined user pays the full bill on time, avoids unnecessary spends, tracks eligible categories, and redeems before points lose value. An undisciplined user may earn rewards and still lose money through interest, late fees, or poor planning.

That is why the best rewards strategy begins with a simple rule. Never spend for points. Spend only when the expense already had a purpose.

Who should use this strategy?

This card strategy fits families who travel at least once or twice a year and are willing to learn how reward transfers work. It is especially relevant for parents who book flights and hotels for multiple people, travel during school holidays, or use airport services often enough for lounges and transfers to replace real costs. It is less suitable for someone who wants direct cash, avoids loyalty programmes, or rarely travels.

There is also a practical caution around eligible spends. Independent card reviews have noted that certain categories such as fuel, utilities, rent, insurance, education, government payments, tax payments, gold, wallet loads, money transfers, cash advances, fees, and charges may not earn reward points, although some may still count towards fee-waiver thresholds depending on terms.

The honest way to read the 28% claim

The HSBC TravelOne rewards 2026 story is exciting because it gives families multiple ways to extract travel value from planned spending. But the 28% claim should be treated as an aspirational outcome, not a fixed entitlement.

It becomes realistic only when three things happen together:

The family spends meaningfully in eligible categories.

The points are transferred to partners where redemption value is strong.

The non-point benefits are actually used instead of being ignored.

If any one of these breaks, the effective return drops. That does not make the card weak. It simply means the user must treat it like a strategy, not a coupon.

The myth is not that 28% value is impossible. The myth is that it happens automatically.

*This is not paid content or a sponsored feature. As part of our finance breakdown series, we are simply analysing one credit card this week to understand how its rewards math works for families.

Pockvue Solutions Private Limited

#1, CRE Spacez, 2nd Floor, 14th Main Road,

Sector 5, HSR Layout, Bengaluru - 560102