The Hidden Gold Tax Disruption Every Indian Parent Needs To Know

A father in Bengaluru opened his demat app one evening and felt relieved to see gold sitting quietly inside his family portfolio. It was not jewellery lying in a locker, not coins bought during a festival, and not a speculative trade bought on impulse. It was a Sovereign Gold Bond, the kind many Indian families had started seeing as the neatest version of gold. Government backed. Linked to gold prices. Carrying fixed interest. And, most importantly in family conversations, believed to be tax efficient on redemption. But the shock was not hidden in the price of gold. It was hidden in a line of tax law most families had never read.

The Comfort Product That Suddenly Needs A Second Look

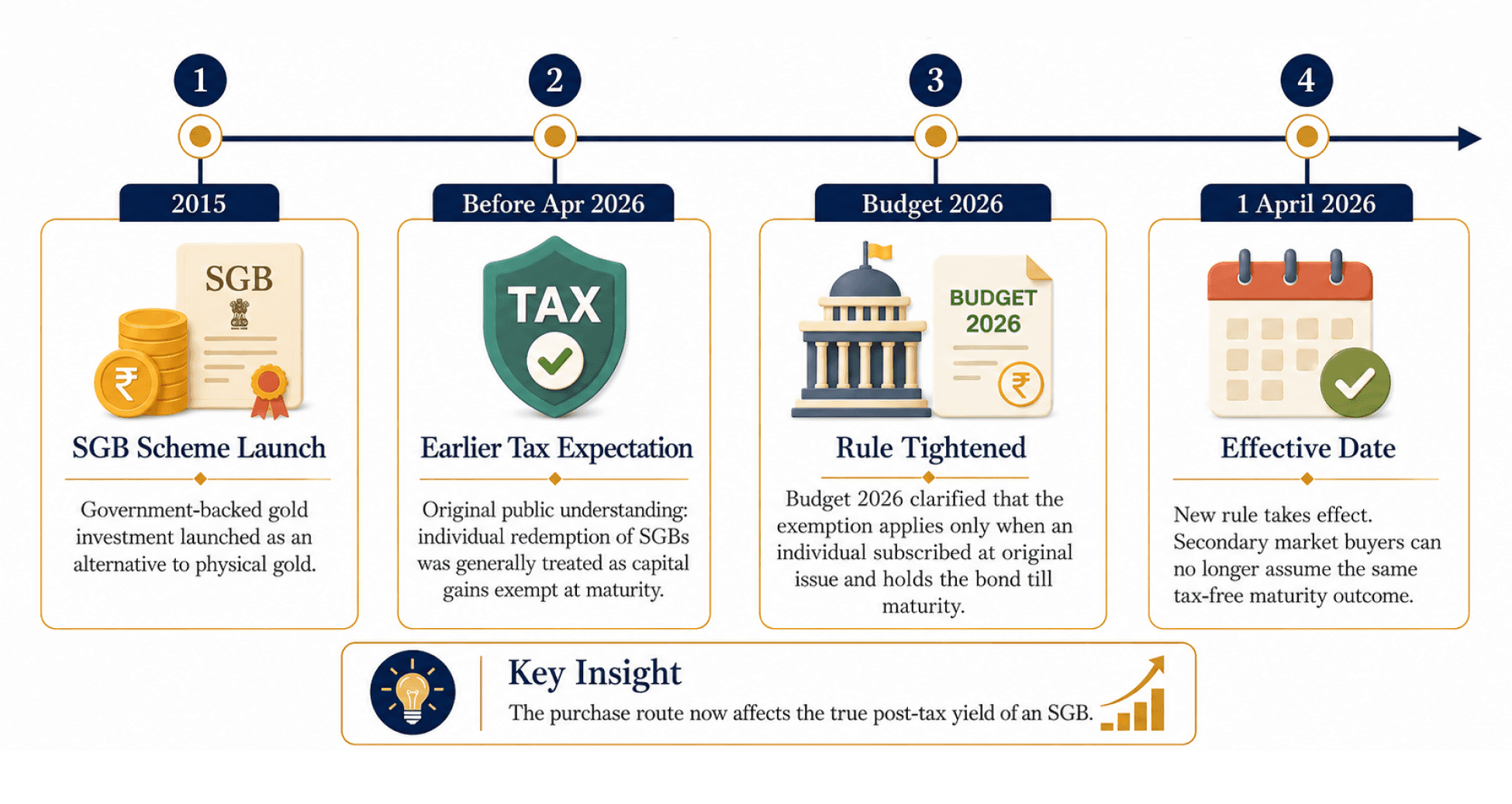

For years, the Sovereign Gold Bond tax 2026 conversation was simple enough for households to remember. SGBs were issued by the Reserve Bank of India on behalf of the Government of India, denominated in grams of gold, redeemable in cash, and designed as a substitute for physical gold. RBI’s public FAQ also explained that the bonds carried 2.50% fixed annual interest on the initial investment, paid semi-annually, while capital gains on redemption to an individual were exempt under the earlier framework. That simplicity is exactly why the new rule feels so unsettling.

The Union Budget 2026 did not say that SGBs are bad. It said something more specific and more important. The capital gains exemption will apply only when the bond is subscribed to by an individual at original issue and held continuously until redemption on maturity. The Budget Speech states this proposed condition clearly, and the Finance Bill places the same idea into the amended wording of Section 70. That one condition changes the way families must classify the same gold asset.

Two Families, One Bond, Two Tax Outcomes

Imagine two parents holding the same SGB series. Family A bought it directly during the original RBI issuance. Family B bought it later through a secondary market portal because it was available at an attractive price. Before this change, many investors assumed that both families could eventually enjoy the same broad maturity benefit. After April 2026, that assumption is no longer safe. The Finance Bill wording says the exemption applies if the SGB is held by an individual from the date of original issue till maturity. This is where secondary market SGB taxation becomes the real story.

The economic lesson here is called asset classification. A product does not carry the same post-tax behaviour for every holder simply because the product name is the same. The Memorandum explaining the Finance Bill says the exemption is intended to be available only where the SGB is subscribed at original issue and held continuously until maturity, and that the amendment takes effect from 1 April 2026 for tax year 2026-27 and later years. This is not merely a tax footnote, because it can change the final number a parent receives.

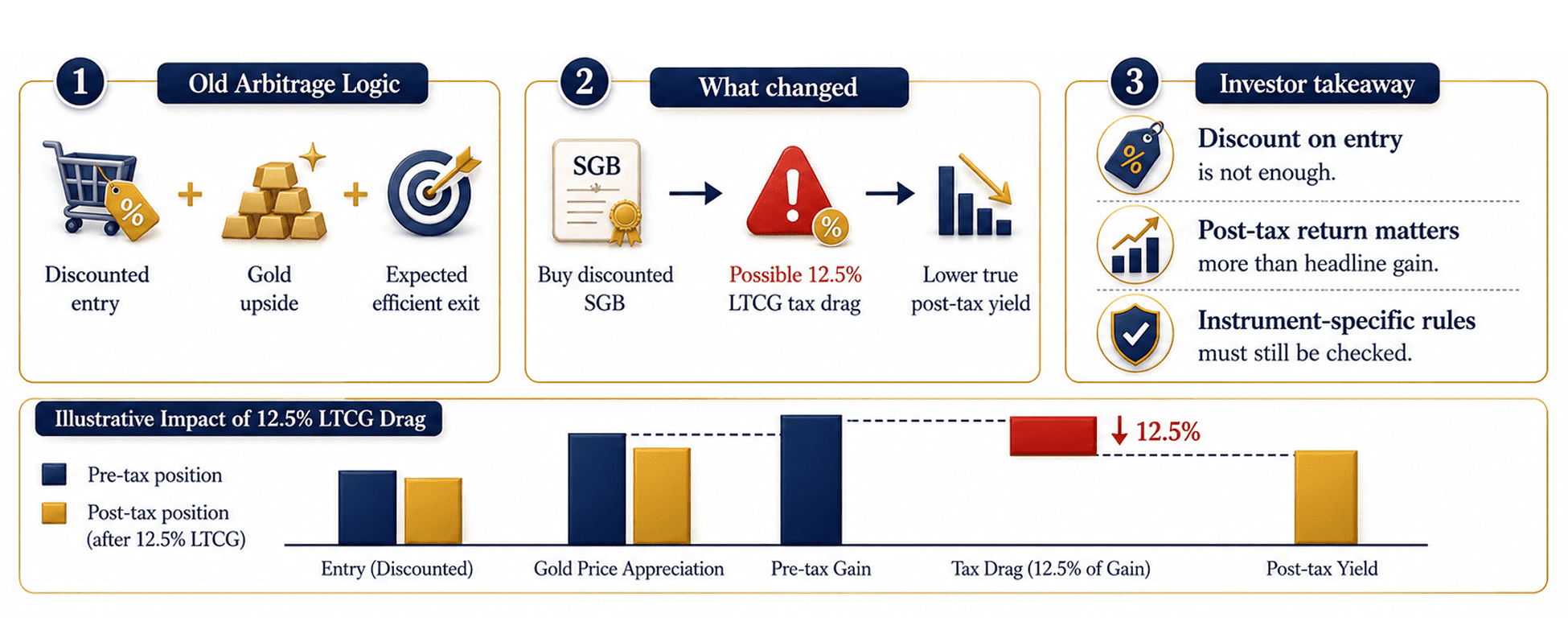

The Tax Arbitrage That Quietly Disappeared

The old attraction of secondary market SGBs was not only gold exposure. It was often the possibility of tax arbitrage. A family could search the exchange for an older SGB series, buy it at a discount, hold it close to maturity, and hope to enjoy gold price appreciation without the same tax burden expected from many other capital assets. RBI confirms that SGBs can be traded on exchanges if held in demat form and can also be transferred to eligible investors. That tradability made the secondary market useful, but it also created the exact situation the new wording now addresses.

Now the purchase route matters as much as the product. If a family buys from the secondary market, the safer assumption is that the maturity exemption may not apply in the same way it applies to the original subscriber. If there is a gain, that gain may need to be examined under capital gains rules, depending on holding period, acquisition cost, redemption value, and the taxpayer’s overall situation. The Income Tax Department’s public guidance says long-term capital gains on many assets transferred on or after 23 July 2024 are taxed at 12.5% without indexation, though the exact treatment should be checked for the specific instrument and facts. The real damage is not panic, but miscalculation.

The True Yield Is No Longer The Displayed Yield

This is where you must stop looking only at gold price growth. A bond bought below its gold value may still look attractive on a screen, but the true yield now needs four layers. First, the price paid. Second, the maturity value linked to gold. Third, the taxable 2.50% annual interest. Fourth, the possible capital gains tax if the investor does not qualify for the maturity exemption. The RBI FAQ already makes clear that interest is taxable under income tax law, even under the old public explanation. The missing calculation now sits inside the capital gain.

For any long-term goal, this matters deeply. Most households do not buy gold exposure because they want excitement. They buy it because it feels steady during inflation, currency weakness, and market uncertainty. But a future goal is not funded by comfort. It is funded by post-tax cash flows. If two investments both rise with gold but one loses part of the gain to tax, the lower true yield can quietly widen the gap between the planned corpus and the actual corpus. That gap is where personal finance becomes real.

The Problem of Education Fund

Many Indian families use gold as emotional insurance. It feels culturally familiar and financially respectable. A grandparent may call it wealth. A parent may call it safety. A child may one day experience it as college fees, hostel deposits, coaching expenses, laptop purchases, or overseas application costs. But when the asset is linked to a goal with a fixed date, the question is not only whether gold will rise. The question is whether the family will receive enough after taxes, transaction costs, and timing risk. That is why SGB tax on maturity is now a planning question, not just a tax question.

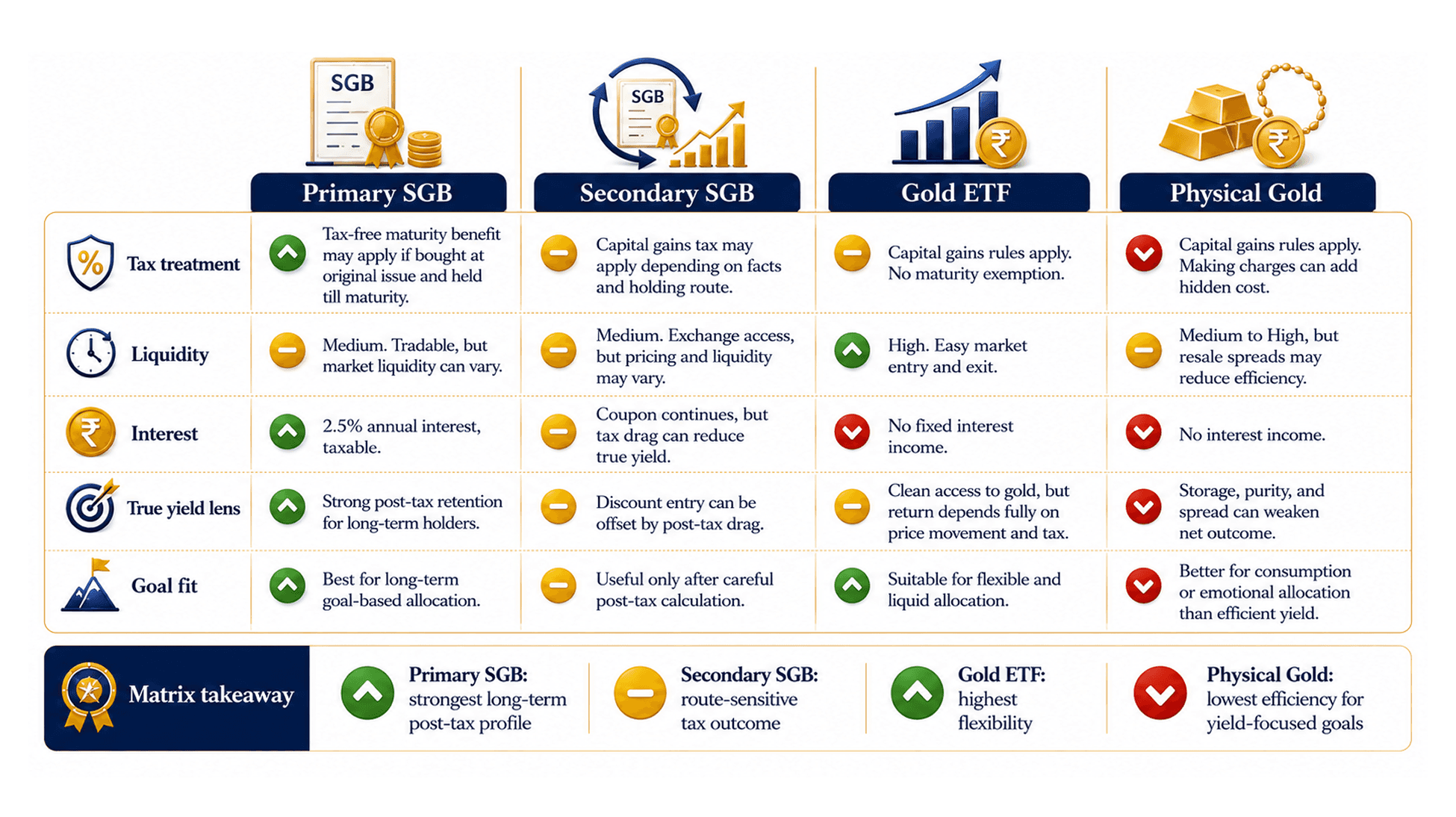

This does not mean people should reject SGBs. It means they should separate primary issue SGBs, secondary market SGBs, gold ETFs, gold mutual funds, physical gold, and diversified funds into different boxes. Each box has a different mix of liquidity, taxation, price behaviour, and emotional comfort. The new rule simply makes this classification more visible. A family that assumes all gold instruments behave alike may end up comparing jewellery, ETFs, and SGBs incorrectly. The next step is to rebuild the comparison table.

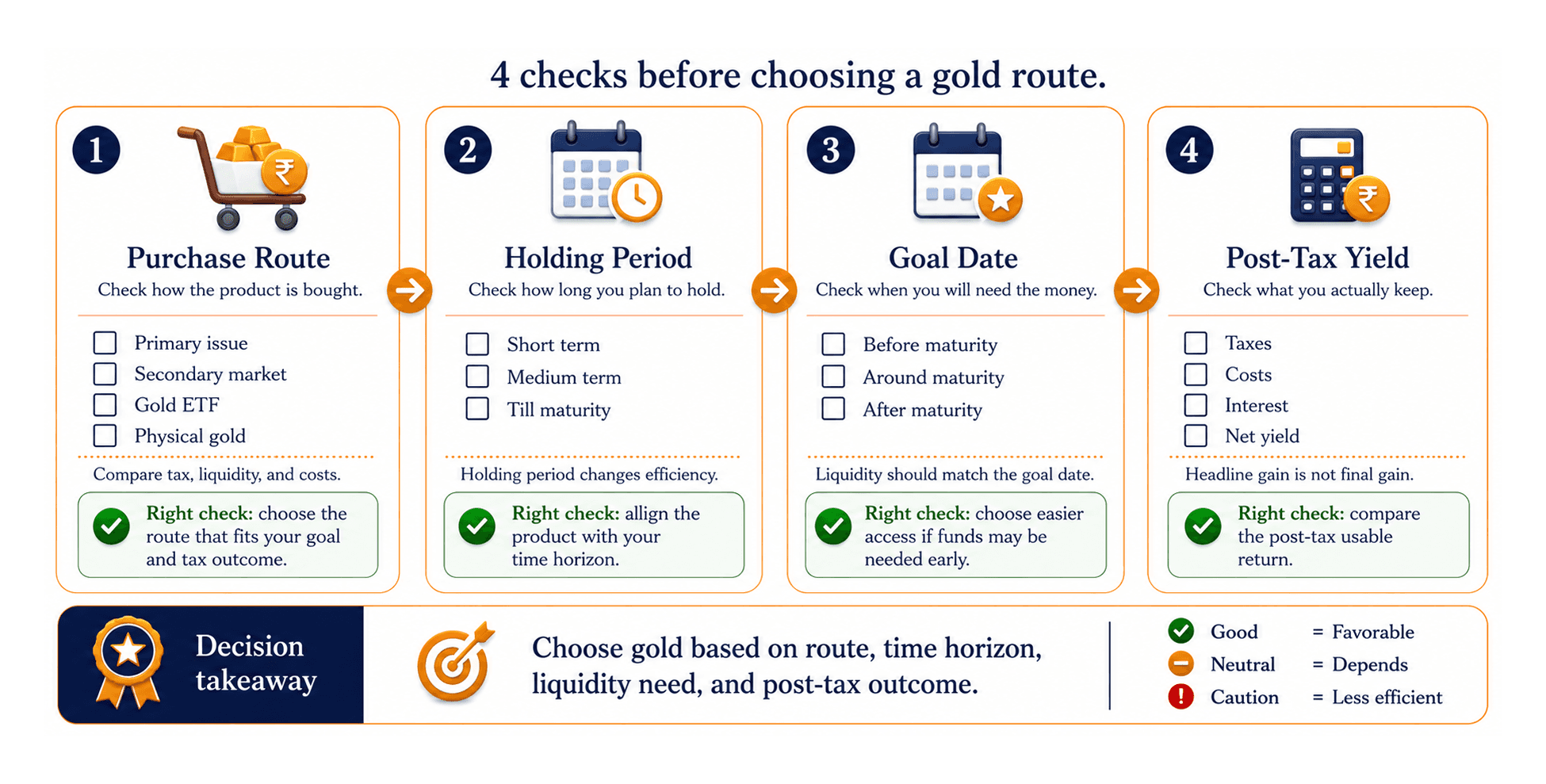

What Parents Should Check Before Buying Gold Now

The first question is simple. Did you buy the SGB at original issue or from the secondary market? The second question is whether you plan to hold it till maturity. The third question is whether your goal needs liquidity before the eighth year. RBI’s FAQ states that the tenor is eight years, with early redemption allowed after the fifth year on coupon payment dates, and that the bonds may be traded on exchanges if held in demat form. These details matter because education expenses rarely wait politely for product maturity.

The fourth question is about post-tax comparison. If a secondary market SGB is available at a discount, the discount must be compared against the possible tax cost. If a gold ETF offers easier liquidity but a different tax pathway, that should be measured too. If physical gold carries making charges, storage concerns, and purity questions, that must also be priced into the decision. The correct question is not “which gold product is best”. The correct question is “which gold product gives the right after-tax cash at the right time”. That answer is rarely found in a headline.

The Safer Way To Use Gold In A Family Portfolio

For a long-term child education portfolio, gold can remain a hedge, not the whole plan. It can protect purchasing power in some periods, balance emotional confidence, and reduce dependence on a single asset class. But it should not be allowed to dominate the portfolio simply because it feels familiar. A family saving for education may still need equity-oriented exposure for growth, debt instruments for stability, liquid funds for near-term payments, and insurance for protection. Gold is one piece of the story, not the full school fee plan.

The April 2026 rule also gives parents a teachable moment. Children often hear adults say that finance is complicated because rules keep changing. But this is exactly why financial literacy matters. A financially aware family does not memorise every section number. It learns how to ask better questions. Who issued the product? How was it bought? When will it mature? What is taxable? What is the post-tax return? What risk is being ignored because the product feels safe? These questions can protect a household better than blind trust.

The New Lesson From The Gold Shock

The hidden lesson of the SGB change is that tax policy can transform the character of an investment without changing its name. The bond still tracks gold. It still comes from the sovereign framework. It still carries fixed interest. But for a secondary market buyer, the old tax-free assumption may no longer hold. The amended Income-tax Act 2025, as updated by the Finance Act 2026, shows the substituted wording and even notes the earlier broader wording that applied to redemption by an individual. That before and after contrast is the clearest proof of the shift.

The conclusion is not fear. It is awareness. If you hold an SGB bought at original issue and plan to hold it till maturity, the benefit may still remain under the new condition. If you bought from the secondary market, do not rely on old explanations without recalculating. If you are buying now for a long-term family goal, compare products by true yield, not by label. Gold may still shine in the portfolio, but after April 2026, the shine must be measured after tax. That is the conversation every investor should have before the next decision begins.

Pockvue Solutions Private Limited

#1, CRE Spacez, 2nd Floor, 14th Main Road,

Sector 5, HSR Layout, Bengaluru - 560102