At 10.45 on a Sunday night, after the plates are cleared, Rajesh is still at the dining table with his brother in law.

The conversation began with school fees. Then, as it often does in Indian homes, it entered the dangerous territory of retirement planning in India. “Buy one small plot near the highway”, the brother in law says. Land never betrays. Rajesh nods. He has heard this before. From his father, his colleague, and the neighbour who sold a flat at the right time.

His wife, Meera, quietly asks whether they should also check their NPS contribution. Rajesh waves the thought away. Not out of arrogance. Out of fatigue. The website feels confusing. The rules feel distant. The returns feel abstract. But the man across the table feels real.

This is how many retirement plans are born in India. Not in a spreadsheet. Not after a structured review. They are born through stories. A property story. A stock story. A fixed deposit story. But retirement does not reward the best story. It rewards the most reliable system.

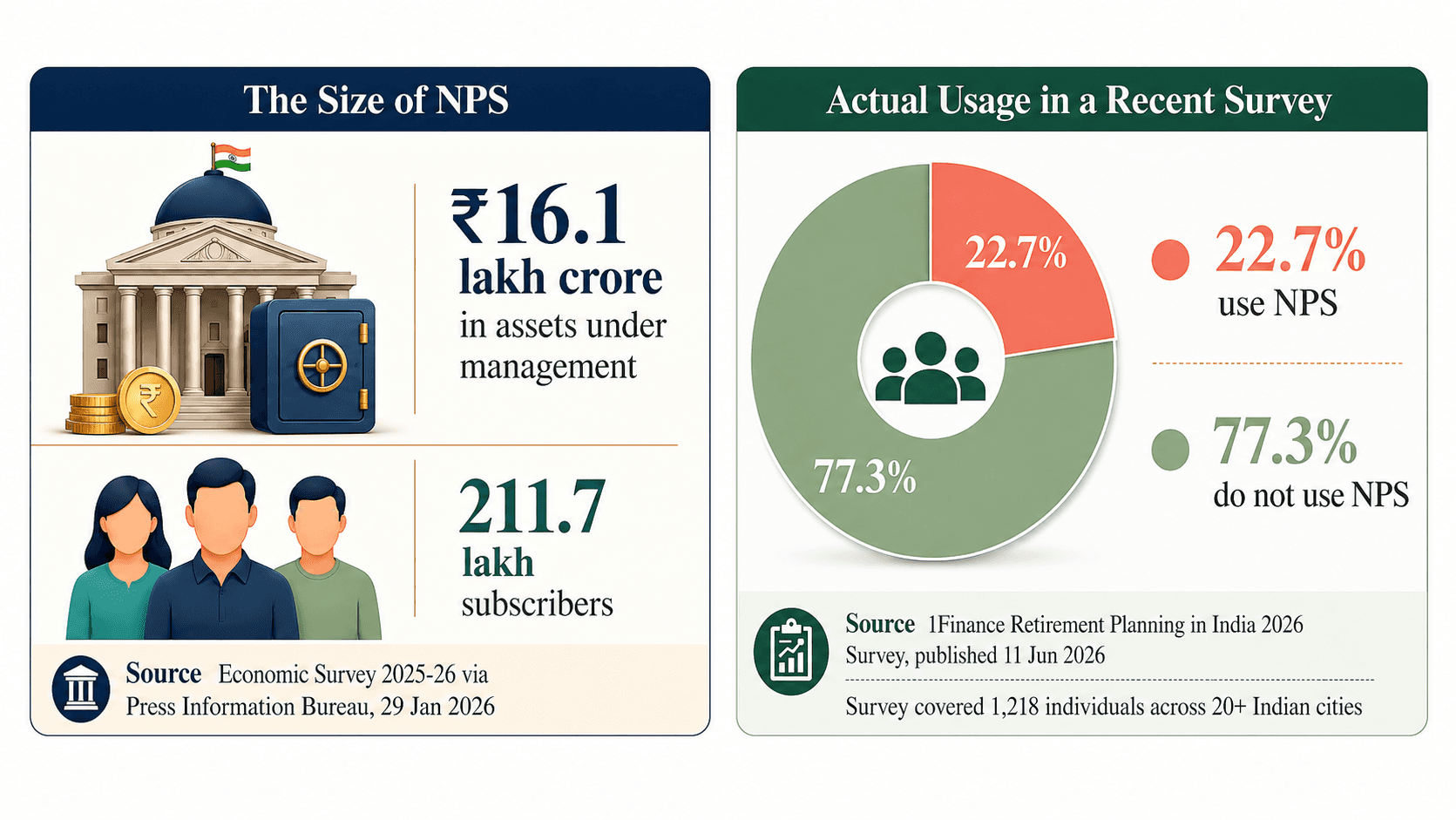

The latest data should make every Indian parent pause. The National Pension System has become one of India’s largest long term savings structures, with assets around ₹16 lakh crore and more than 2 crore subscribers. Yet in a recent retirement survey, only 22.7 percent of respondents said they actually use it.

A large national retirement machine exists. But only about one in four surveyed people are sitting in it.

The National Pension System vault most families walk past

Imagine a giant savings vault in the middle of the city. It has formal rules, regulated managers, digital access, tax advantages for many users, and one job. To help working Indians collect retirement money brick by brick.

Now imagine lakhs of families walking past that vault every day and asking a relative where to keep their future. That is the emotional contradiction of NPS for retirement in India.

NPS is not magic. It is a structured vehicle. Think of it like a disciplined school bus for your future money. You still have to board it and choose the route. But it is designed to move in one direction over many years, instead of chasing fashionable ideas.

The problem is that most families do not experience NPS as a school bus. They experience it as a government form. A story from a friend feels warm. A government platform feels cold. A relative’s property tip comes with chai and confidence. NPS comes with login pages, fund options and withdrawal rules. One feels like human trust. The other feels like institutional trust.

For decades, money decisions in Indian homes were built around lived proof. Parents trusted the uncle who bought land early, the aunt who bought gold every Diwali, and the colleague who got insurance through an agent. Many households grew up with advice that travelled through relationships.

So when a system like NPS asks for trust without a human face, many people hesitate. The strange part is that the same families who want stability for their children often delay using the very infrastructure designed for long term retirement savings. They do not ignore it because they are irresponsible. They ignore it because it does not feel familiar enough.

The hidden cost of trusting only family and friends

The retirement survey found that 76.9 percent of respondents plan retirement without professional help. Family and friends were the primary source for 49.5 percent, far ahead of financial advisors. This is where the real danger begins.

Family advice can be caring. It can also be incomplete. A friend may know what worked for him. He may not know what works for you. Your colleague’s stock tip does not know your daughter’s higher education plans. Your uncle’s property belief does not know your medical responsibilities. Your neighbour’s fixed deposit comfort does not know how inflation can shrink purchasing power over twenty years.

Inflation is like a slow leak in a water tank. Nothing dramatic happens, yet the level keeps dropping. Retirement works the same way. A plan that looks safe today can become weak if it cannot keep pace with future prices.

This is the friend and family financial penalty. It is not a visible fee. No one sends you a bill for it. It appears later as a smaller retirement corpus, delayed retirement, pressure on children, or sudden compromise in lifestyle.

Rajesh feels this when he opens his bank statement at midnight a week after the dinner conversation. His salary looks healthy. His savings look respectable. His EPF is growing. There are two fixed deposits, some gold, a few mutual funds, and one insurance policy he barely understands.

On paper, he feels responsible. But when Meera asks one simple question, the confidence shakes. Will this be enough when we are sixty? That question cannot be answered by confidence. It needs numbers.

It needs a retirement corpus estimate. It needs a clear view of future expenses. It needs a way to compare NPS, EPF, PPF, mutual funds, deposits and insurance without emotion. It needs a plan that does not change every time someone tells a new story at dinner.

Why salaried professionals hesitate to trust the blueprint

Many Indian parents are not avoiding formal retirement systems because they are careless. They are avoiding them because the systems do not feel emotionally easy to trust.

First, abstract money feels less real than physical assets. A plot can be visited. Gold can be touched. A flat can be shown to relatives. NPS units live behind a screen. For a generation trained to value what can be seen, this matters.

Second, complexity creates distance. Terms like asset allocation, annuity, Tier 1 and pension fund manager make many people step back. After a full day of work, parenting, traffic and bills, no one wants their future to feel like homework.

Third, government infrastructure often carries emotional baggage. Many families associate official systems with queues, forms and confusion. Even when the digital version is smoother, the older feeling remains.

Fourth, social proof beats data. If three people in your circle say property is best, it feels more convincing than a chart showing the growth of a pension system.

This is why trust has to be rebuilt step by step. Not by telling parents they are wrong. By showing them that verified systems can sit alongside their instincts, not insult them.

For a 35 plus salaried professional, retirement planning is not just about finding the best investment. It is about building a retirement track that can survive changing markets, rising medical costs, tax changes, family needs and longer life expectancy.

NPS should not replace all family wisdom. It should be understood as one part of a larger retirement blueprint. The point is not to stop listening to people. The point is to stop allowing casual conversations to become the entire plan.

A simple transition guide for professionals above 35

If you are 35 or older, the goal is not to panic. The goal is to move from scattered confidence to structured clarity.

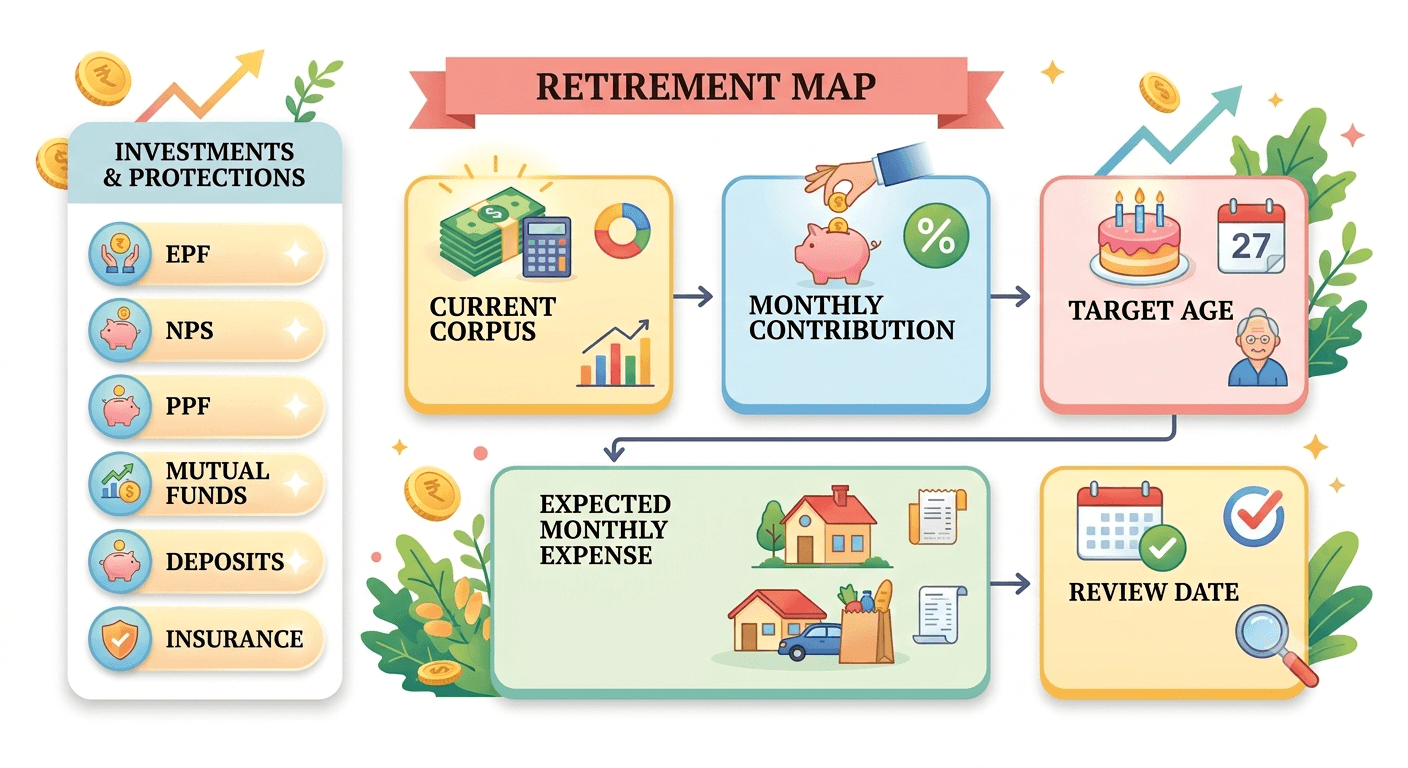

Start with a retirement inventory. Write down every asset meant for your future. EPF, PPF, NPS if any, mutual funds, fixed deposits, gold, property, insurance surrender values, and cash. Do not judge the list. Just gather it.

Then separate emotional assets from retirement assets. The house you live in may give security, but it may not pay monthly expenses. Gold may help in emergencies, but it is not a full pension plan. A plot may be appreciated, but it may not be easy to sell when you need money.

Next, calculate your future expense anchor. Take today’s monthly household expense and ask what part will continue after retirement. Food, utilities, healthcare, travel, maintenance, insurance and support for parents or children may remain. School fees may go away, but medical costs may rise.

After that, review the National Pension System without emotion. Ask simple questions. Are you eligible? How much tax benefit applies to you? How much can you contribute regularly? Which allocation suits your age and risk comfort? How does it fit with EPF, PPF and mutual funds?

This is also where NPS tax benefits should be understood properly. Not as the only reason to invest, but as one possible advantage in a larger retirement plan. A tax saving product is useful only when it also supports your long term goal.

Then speak to a qualified advisor. Not someone who only wants to sell a product. A good financial advisor for retirement planning should ask about income, debt, dependents, retirement age, health cover, goals and existing investments before suggesting anything.

Finally, create a one page retirement map. It should say how much you have, how much you need, where the money will come from, how much you will invest every month, and when you will review it. This one page is more powerful than ten dinner table opinions.

The retirement circle every Indian family needs to audit

The best retirement circle is not made only of people who love you. It is made of people and systems that can protect your future. So test your current retirement circle with five questions.

Does this person know my complete financial picture?

Can this advice be verified through an official source?

Does this product solve a retirement need or only feel familiar?

Have I compared cost, liquidity, tax impact and risk?

Would I still follow this advice if it came from a stranger?

If the answer is mostly NO, your plan may be running on trust without structure.

That does not mean you must reject family wisdom. Indian families have survived because they share knowledge, warnings and experience. But retirement is too important to outsource to whoever speaks with the most confidence after dinner.

Rajesh does not need to fight with his brother in law. He does not need to abandon property, gold or fixed deposits overnight. He simply needs to stop treating every familiar story as a financial blueprint.

The real shift is gentle but powerful. Listen to people. Verify with data. Build with systems. Review with professionals. Decide as a family. That is how trust becomes protection.

NPS usage at 22.7 percent is not just a statistic. It is a mirror. It shows that India does not merely have a retirement awareness problem. It has a retirement trust problem.

And for parents in their late thirties, forties and fifties, the lesson is urgent. The future will not ask whether your advice came from someone sincere. It will ask whether the plan was strong enough.

Pockvue Solutions Private Limited

#1, CRE Spacez, 2nd Floor, 14th Main Road,

Sector 5, HSR Layout, Bengaluru - 560102